Convenience and flexibility are indeed reasons to appreciate credit cards, but the potential to make one fall into substantial debt has oftentimes been underestimated. One of the most common mistakes credit card users make is paying only the minimum amount due.

The minimum payment may seem manageable, but it ends up costing much more than you realize. Understanding the true cost of paying only the minimum can help you make better financial decisions and avoid unnecessary debt.

The Long-Term Effects of Minimum Payments

Minimum payments can negatively affect your long-term financial health. Understanding how these effects arise can enable you to take steps to decrease the cost and more favorably manage your credit card debt.

Increased Debt Over Time

As mentioned earlier, making only minimum payments increases your overall debt due to accumulating interest. With this in mind, any financial goals are hardly reachable, such as retirement savings or buying a house.

The longer it takes you to pay off your credit card debt, the more you're gonna build up in interest, and that interest is what could stand in your way from building wealth and reaching financial stability.

Additional Fees Accumulation

This may also lead to credit card companies charging you extra fees if you continue to pay the minimum amount. The additional Late fees, over-limit fees, and all other charges may also increase your balance more and, therefore add to the debt burden that is growing.

These additional charges make it even harder to pay off your debt, creating a cycle of growing financial strain.

Legal Consequences

In extreme cases, failing to make more than the minimum payments can lead to severe legal consequences. If your debt becomes significantly overdue, you may face a credit card debt lawsuit. Credit card companies may take legal action to recover the money owed, leading to court judgments, wage garnishments, or other legal repercussions.

Addressing credit card debt proactively can help you avoid such situations and maintain better control over your financial health. You will be in a better position to avoid this type of situation and be in a stronger position with regard to your financial health by being more proactive toward credit card debt.

The Cost of Paying Only the Minimum

With just the minimum payment on your card, you are paying merely a small percentage of your whole outstanding balance. Credit card companies typically charge a minimum payment as a small percentage of your outstanding balance, plus interest and fees.

This surely makes the repayments look cheaper but the fact is that you are elongating your debt and with this process, you will pay much more over time than you need to.

Interest Accumulation

Most credit cards have extremely high interest rates, from 15% upwards to 25% or even more. At these high rates, with a minimum payment, most of that goes toward interest, not to pay down the principal.

As a result, interest builds up quickly and compounds over time, significantly slowing down your debt repayment. This circle of interest accrued can at times inflate the total amount owed to great heights, doubling or even tripling the amount borrowed in the process.

Extended Repayment Period

Paying only the minimum also extends the time taken to pay off your credit card balance. At a balance of $5,000 on a 2% minimum payment and 20% interest rate, the debt could take well over 15 years to pay off if you are paying the minimum.

Over this time, you will have paid a considerable amount in interest, thus making you pay a lot more than what you originally purchased.

Lowered Credit Score

High credit card balances, in relation to your credit limit, are bad for your credit score. When you make only the minimum payment, your balance stays high, which raises your credit utilization ratio- the percentage of credit you are using compared with the total amount of credit available to you.

When your credit utilization ratio is high, it can adversely affect your credit score, thereby making it harder for you to get a loan or get the best interest rates later.

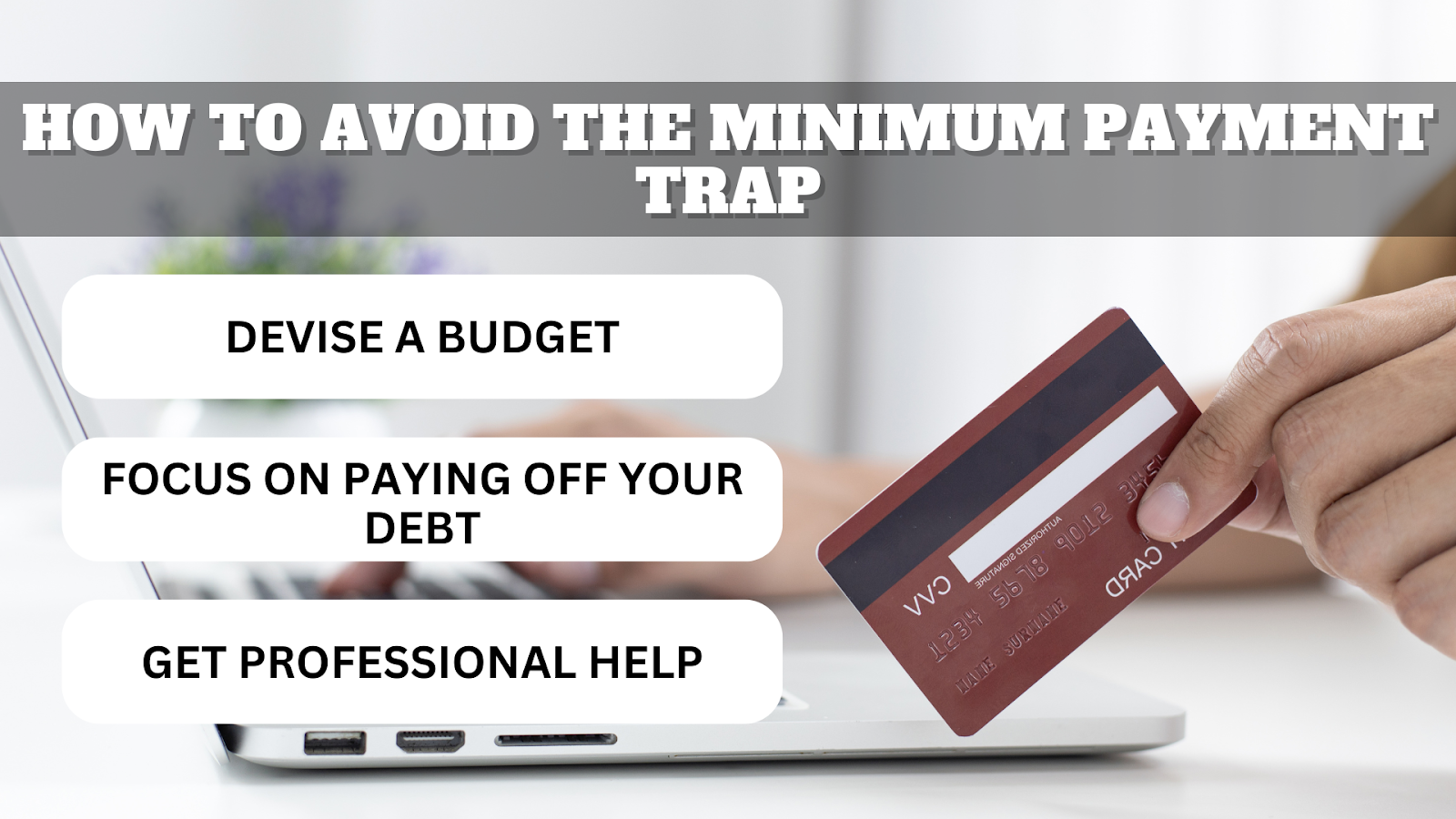

How to Avoid the Minimum Payment Trap

Here are some strategies that will help you avoid minimum payment pitfalls on your credit cards:

-

Devise a Budget: Having a detailed budget can support your attempt to manage your expenditure in a better way and bring about a certain assurance that you'll be earmarking enough money toward debt settlement of your credit card balances.

-

Focus on Paying Off Your Debt: Pay off your credit card debt on priority. You may try the avalanche or snowball method to pay off your debt efficiently. In the avalanche method, you prioritize paying off high-interest debt first. On the other hand, you need to pay the small balances first when you use a snowball method.

-

Get Professional Help: If you have some problems with credit card debt, consider consulting a financial consultant or credit counselor. These professionals can advise on dealing with debt, including making a plan for repaying debt and improving one's finances generally.

Conclusion

While just making the minimum payment on credit cards might ease life, there are a lot of long-term costs involved with that. From incurring expensive interest charges to prolonging repayment and even possible legal consequences, making minimum payments has serious repercussions.

By realizing these effects and making use of techniques that pay off your debts better, you'll be in a position to take charge of your finances and avoid minimum payments. The upside: taking action now means better financial health and peace of mind later.

FAQs

-

Why does paying only the minimum on credit card charges cost more over time?

When only the minimum amount is paid, there is a higher amount of interest levied and it will take longer to pay, so one pays much more over time.

-

What is a credit card debt lawsuit?

A credit card debt lawsuit is a legal action that a creditor has taken to recover an overdue debt owed by a borrower, usually resulting in court judgments along with any other legal ramifications.

-

How can I pay off my credit card debt faster?

You will be able to pay off your credit card debt faster if you pay more than the minimum, focus on the balance with the highest interest, and budget to keep your finances in order.